Focus on Lease Accounting: Scope and Lease Definition

Focus on Lease Accounting: Scope and Lease Definition

New lease accounting rules will be effective January 1, 2022 for private companies with a calendar year end. The Financial Accounting Standards Board (FASB) undertook this project with the International Accounting Standards Board in 2006 and issued a final standard, Accounting Standards Update 2016-02 (ASU), in 2016. The FASB has since issued a number of amendments to provide clarifications and to delay the effective date. All of these updates are codified in Accounting Standards Codification Topic 842, Leases. Public companies have already adopted the new standard. After a number of deferrals, the effective date for private companies is fiscal years beginning after December 15, 2021.

Under this ASU, a lessee will be required to recognize on its balance sheet an asset and a liability for all leases that have a term of more than 12 months, with a practical expedient for shorter leases. Recognition, measurement, disclosure and presentation of cash flows will be determined by whether the lease is either a financing lease or an operating lease.

Under both types of leases, the lessee will be required to recognize a right of use asset and a lease liability, measured at the present value of the lease payments. For financing leases, interest on the lease liability will be recorded separately from amortization of the right to use asset. Repayments related to the principal will be treated as financing cash flows and interest payments will be recorded within operating activities on the statement of cash flows. Under operating leases, the lessee will record a single lease cost calculated so that the cost of the lease is recognized over the lease term on a generally straight-line basis. All cash payments under these operating lease agreements will be categorized as operating cash flows. The new standard also includes expanded disclosure requirements.

Lessor accounting will remain primarily unchanged under this new ASU. Recent pronouncements over revenue recognition have been considered in the development of this topic in an effort to ensure more consistency.

The implementation of the new standard is expected to be a significant undertaking for entities that have more than a handful of leases. While there may not be a significant impact to earnings, most entities will have a significant change to their balance sheet and a number of new disclosures, both qualitative and quantitative.

Lease Definition

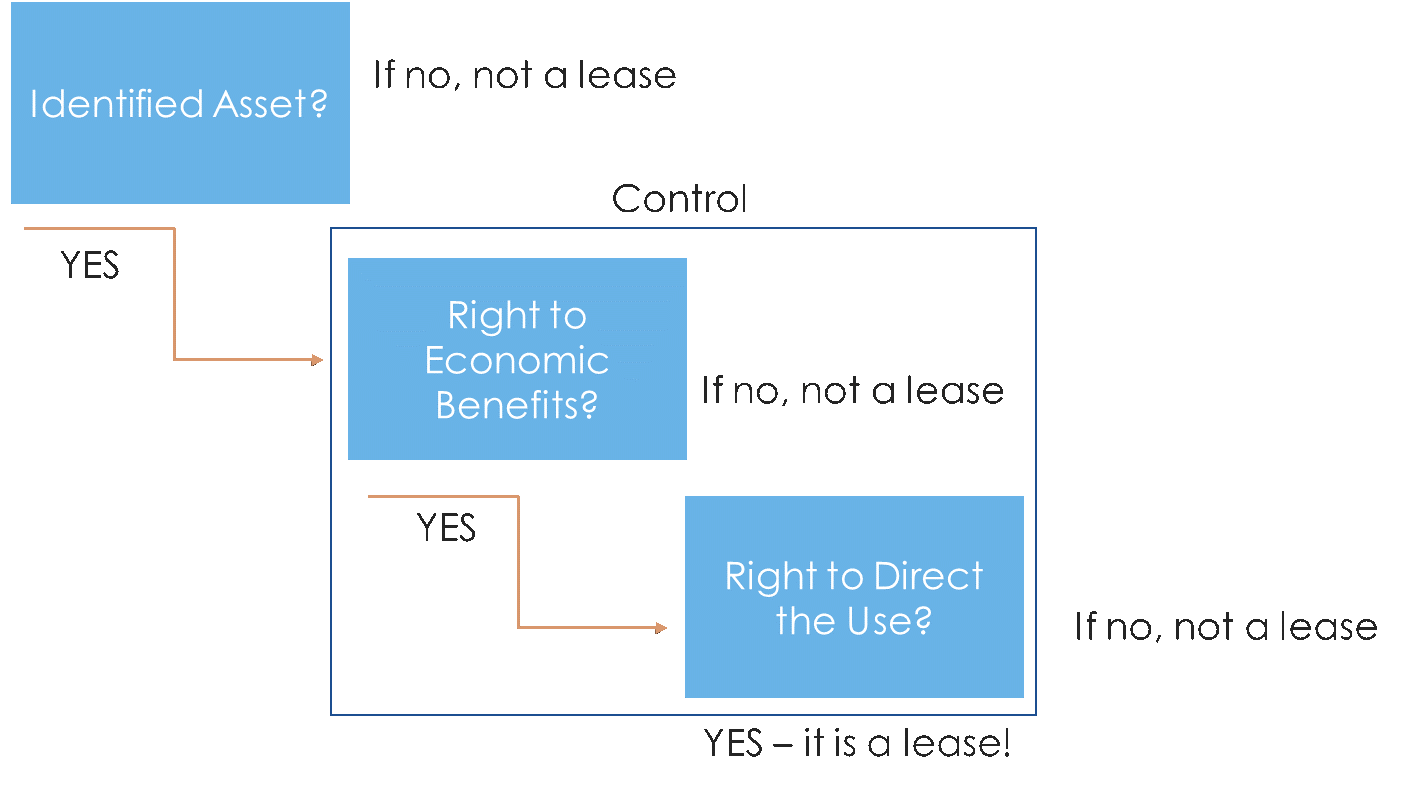

The new standard creates a new definition of a lease that uses the concept of control. A lease is defined as a contract, or part of a contract containing an embedded lease, that conveys the right to control the use of an identified piece of property, plant, or equipment (an identified asset) for a period of time in exchange for consideration. ASC 842 excludes leases of:

- Intangible assets

- Exploration for minerals, oil, natural gas, etc.

- Biological assets, including timber

- Inventory

- Assets under construction

A lease includes an asset that is identifiable, either explicitly or implicitly (e.g. the only asset that can satisfy the contract). The asset can be specifically identified in the contract. An asset is implicitly identified if only one asset can be used to fulfill the contract or if the rights in the contract represent substantially all of the capacity of the asset. If there is no identified asset, there is no lease.

Overview of lease definition:

While this seems like a straightforward analysis, other considerations can make the determination more complicated. A physically distinct portion of a larger asset could represent a specified asset, but a capacity portion of a larger asset will generally not represent a specified asset. If a contract permits substitution, it does not have an identified asset. But, if the supplier cannot readily obtain a substitute or it would not be economically beneficial for the lessor to make the substitution, there is an identified asset. The standard provides several examples to illustrate these concepts.

Consider this scenario; a commercial bank enters into a data center contract. The supplier has multiple interchangeable data centers, but due to required security parameters, specific restrictions are imposed by the bank on the equipment. In this case, even though the assets used to fulfill the contract are not explicitly stated, the assets are implicitly identified as a result of the contractual requirements and specifications mandated by the bank.

In another example, a Warehousing Corp. owns a warehouse that can be subdivided. Manufacturing Corp. reserves 1,000 square feet to store inventory for 3 years at a specified location. Warehousing Corp. can shift the inventory location at its discretion. Assuming that 1,000 square feet is only a small portion of a larger warehouse, there is no identified asset. The supplier can shift the inventory at its discretion and it is reasonable to assume that it would be economically beneficial for supplier to do so.

Once you conclude that the contract includes an identified asset, the next step is to determine who has control of the asset. A customer controls an identified asset when the customer has both the right to obtain substantially all of the economic benefits from its use and the right to direct its use.

The right to obtain substantially all of the economic benefits refers to only the benefits that arise from use of the asset, not from ownership. Only the benefits that result from the defined scope of the customer’s right to use the asset in the contract are considered in making the determination.

The right to direct its use means that the customer has the right to direct how and for what purpose the asset is used for the defined period. If the relevant decisions about how and for what purpose are predetermined by the contract, then the customer has the right to direct the use of the asset when it has the right to operate or to direct others to operate as it determines without the supplier having the right to change operating instructions. A customer is also considered to direct the use if it designed the asset in a way that predetermines how and for what purpose the asset will be used.

To illustrate these concepts consider these examples provided in the standard.

Example 1A

Contract provides use of 10 railcars for 5 years

- Railcars specified, owned by freight carrier (Supplier)

- Customer determines when, where, and what goods are to be transported (except for specified hazardous materials)

- Cars not in use kept at customer premises

- Supplier cannot retrieve cars except for repairs

- Supplier provides engines and drivers on request

This contract contains a lease. There are ten specifically identified railcars. The restriction on cargo is protective and does not affect the right to direct the use of the asset. These types of restrictions on use define the right of use, but are not necessarily indicative of control.

Example 1B

Supplier transports specified quantity of goods using specified type of cars for 5 years

- Supplier provides railcars, driver, and engine

- Customer determines when, where, and what good are to be transported

- Contract states nature/quantity of goods

- Supplier has large pool of cars that can be used

- Cars and engines stored at Supplier’s premises

This contract does not contain a lease. There is no identified asset. The customer has a right to a specified capacity and the supplier has the right to select which specific assets it uses to fulfill that capacity. Additionally, a pool of cars at the supplier’s location indicates that the supplier has the ability to substitute at little or no cost in a way that is economically beneficial.

Other Scope Considerations

The standard is generally applied at the contract level. However, the standard does provide for the use of a portfolio approach but only in situations where the leases are for a group of homogenous assets that have identical or nearly identical lease terms. The application of the accounting model to the portfolio should not differ materially from the application of the model to the individual leases. We expect the use of the portfolio approach to be limited in practice to vehicle fleets and computer hardware / copiers. Entities should apply judgement in selecting the size and composition of the portfolio, specifically considering differences in assets, lease term and commencement dates. Additionally, the FASB specified that the approach is not available for leases of real estate.

In most cases, we expect the determination of whether a contract includes a lease to be a straightforward exercise that results in similar answers as under legacy GAAP. However, some of the considerations in the new standard, like substitution rights and control, can be complex and require significant judgement.

In the next installment, we will address the recognition and initial measurement of the lease contract.

Readers should not act upon information presented without individual professional consultation.

Published: 06/14/2021

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.