COVID-19: Small Business Administration Publishes Frequently Asked Questions Regarding PPP Loan Forgiveness

COVID-19: Small Business Administration Publishes Frequently Asked Questions Regarding PPP Loan Forgiveness

RubinBrown continues to closely monitor both the SBA and congressional activity around PPP. We plan to hold a webinar in the coming weeks recapping the PPP forgiveness process once Congress settles on any additional PPP legislation. Borrowers should remember they have until 10 months after the end of the loan’s covered period to submit their PPP loan forgiveness application. Due to the complexity of the forgiveness process, the goal of maximizing forgiveness and penalties for incorrect applications, borrowers should carefully review all applicable guidance before submitting their loan forgiveness application. RubinBrown has developed a suite of services to assist borrowers through this process.

On August 4, 2020, the Small Business Administration (SBA) published 20 new Frequently Asked Questions (FAQs) governing forgiveness of Paycheck Protection Program (PPP) loans. While the FAQs largely reinforced rules established by the PPP Flexibility Act – signed into law on June 5, 2020 – and published in previously released Interim Final Rules, there were several new clarifications within the FAQs that are worthy of note. These items are discussed below.

Required Repayments of Principal and Interest Prior to Forgiveness Determination

If a borrower submits its loan forgiveness application within 10 months of the completion of the covered period, the borrower is not required to make any payments until the forgiveness amount is remitted to the lender by the SBA. If the loan is fully forgiven, the borrower is not responsible for any payments. If only a portion of the loan is forgiven, or if the forgiveness application is denied, any remaining balance due on the loan must be repaid by the borrower on or before the maturity date of the loan. Interest accrues during the time between the disbursement of the loan and SBA remittance of the forgiveness amount. The borrower is responsible for paying the accrued interest on any amount of the loan that is not forgiven. The lender is responsible for notifying the borrower of remittance by the SBA of the loan forgiveness amount (or that the SBA determined that no amount of the loan is eligible for forgiveness) and the date on which the borrower’s first payment is due, if applicable

Treatment of Non-Cash Compensation

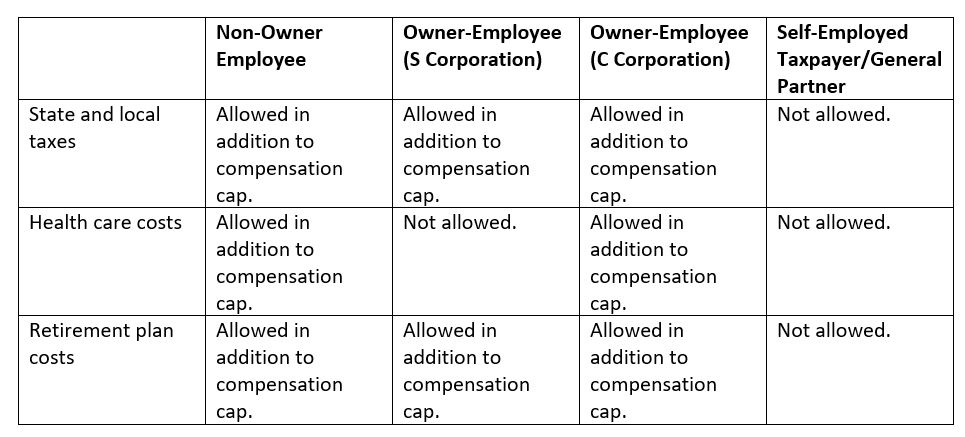

The amount of compensation of owners who work at their business that is eligible for forgiveness depends on the business type and whether the borrower is using an eight-week or 24-week covered period. If a 24-week period is used, the amount of loan forgiveness requested for owner-employees and self-employed individuals’ payroll compensation is capped at $20,833 per individual in total across all businesses in which he or she has an ownership stake. For borrowers that received a PPP loan before June 5, 2020 and elect to use an eight-week covered period, this cap is $15,385. For owner-employees of S corporations or C corporations, the payroll costs are further limited to 2.5 months of 2019 cash compensation (or 8 weeks if the 8-week covered period is elected). For self-employed taxpayers and general partners, the forgiveness amount is determined based on 2.5 months (or 8-weeks, if elected) of 2019 net income from self-employment.

In addition to cash compensation, borrowers are generally eligible to have forgiven the following costs: 1) employer state and local taxes paid on compensation, 2) employer contributions for employee health insurance, and 3) employer contributions for employee retirement plans.

Until the issuance of the recent FAQs, it was not clear which non-cash compensation expenses owner-employees and self-employed taxpayers would be eligible to have forgiven, and whether those costs would be subject to the caps discussed above. Based on the FAQs, however, the following conclusions can be reached:

Treatment of Renewed Leases and Refinanced Mortgages

Payments made on recently renewed leases or interest payments on refinanced mortgage loans are eligible for loan forgiveness if the original lease or mortgage existed prior to February 15, 2020. Similarly, if a mortgage loan on real or personal property that existed prior to February 15, 2020 is refinanced on or after February 15, 2020, the interest payments on the refinanced mortgage loan during the covered period are eligible for loan forgiveness. Example: A borrower entered into a five-year lease for its retail space in March 2015. The lease was renewed in March 2020. For purposes of determining forgiveness of the borrower’s PPP loan, the March 2020 renewed lease is deemed to be an extension of the original lease, which was in force before February 15, 2020. As a result, the lease payments made under the renewed lease during the covered period are eligible for loan forgiveness.

Definition of “Transportation Expenses”

Covered utility payments, which are eligible for forgiveness, include a “payment for a service for the distribution of . . . transportation.” A service for the distribution of transportation refers to transportation utility fees assessed by state and local governments. Payment of these fees by the borrower is eligible for loan forgiveness.

Determining Whether an Employee has had Salary Reduced within the Covered Period

When calculating whether a borrower has reduced the salary of an employee during the covered period in excess of 25% of the annualized salary paid to the employee during the first quarter of 2020, the first quarter annualized salary does not include bonuses, but rather only salaries and wages.

By: Tony Nitti, CPA, MST

Partner-In-Charge

National Tax

609.658.9593

tony.nitti@rubinbrown.com

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.

Published: 08/13/2020

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.