Focus on Business Interruption: COVID-19 Lawsuits and Legislative Developments

Focus on Business Interruption: COVID-19 Lawsuits and Legislative Developments

As stated in our business interruption piece on March 24, 2020, the global impacts of the COVID-19 pandemic have caused economic losses to businesses and individuals throughout the world, resulting in litigation and regulatory activity within state governments and the federal government. Changes in consumer behavior due to COVID-19 and government-ordered shutdowns to quarantine and contain the spread of the outbreak have negatively impacted businesses across several sectors causing many business owners and lawmakers to explore remedies for economic relief.

Business owners searching for relief should review their insurance policies and familiarize themselves with any business interruption insurance coverage they may possess.

Several business owners with insurance policies providing some form of business interruption coverage have filed claims that have been denied by their insurance companies. Many insurers are denying these claims, including claims made under Civil Authority clauses due to government mandated shelter-in-place orders and/or shutdowns, under the predicate that the policy has a virus exclusion, or that viruses are not a covered cause of loss. Many insurers are also taking the position that the damage was not “physical damage,” and insurance policies often require physical damage to trigger coverage.

The insurers’ denials of coverage have caused a number of policyholders to file complaints against their insurers. The businesses seek to win lawsuits that would force insurers to provide coverage for their respective policies. The first lawsuit originated in New Orleans, Louisiana,1 which was followed by other businesses filing lawsuits across the country. Many of the policyholders filing lawsuits held insurance policies that do not include a virus exclusion. As of the date of this article, courts within the United States have not issued any judgements in these cases.

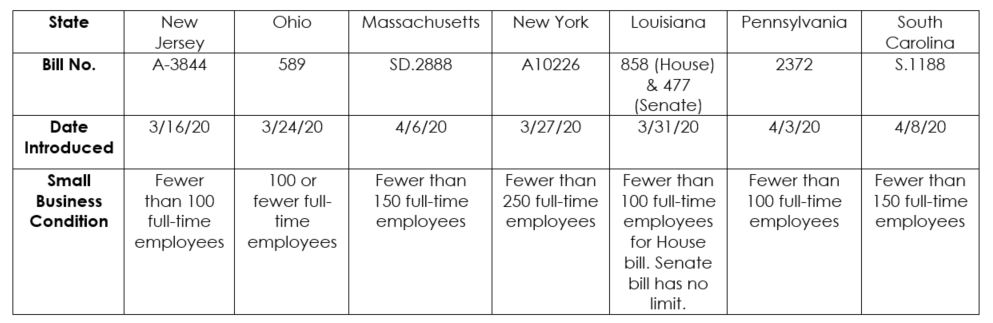

Further, state governments initiated the first wave of business interruption related legislation to debate measures that would help business owners potentially receive compensation from their insurers. New Jersey was the first state to introduce legislation on March 16, 2020,2 which would require insurers to compensate policyholders that suffered business interruption losses as a result of COVID-19. Further, six additional states introduced legislation that would require insurers to provide coverage for certain policyholders that suffered business interruption losses due to COVID-19. The states that have introduced legislation include New Jersey,3 New York,4 Pennsylvania,5 Louisiana,6 Ohio,7 Massachusetts,8 and South Carolina.9 The state bills are currently in the committee stage of the legislative process, with the exception of New Jersey, which was tabled after entering the committee stage.10 The bills require that business interruption coverage be mandated for small businesses that have a conditional number of employees, as illustrated in the figure below.

Also, the federal government introduced a bill on April 14, 202011 called the Business Interruption Insurance Coverage Act of 2020. The bill would mandate coverage for all business interruption policies and prevent the denial of claims due to major events like viral pandemics, forced closure of businesses, mandatory evacuations, and public safety power shutoffs.12 This bill allows insurers to deny coverage if premiums have not been paid. It does not specify that businesses must keep their staff employed or continue to cover their health insurance. Insurers have been critical of both the federal and state government bills; they state that the mandated coverage would result in ripple effects to the economy and could result in the insolvency of many insurance companies. The bill was referred to the House Committee on Financial Services at the time of writing.13

Also, the federal government introduced a bill on April 14, 202011 called the Business Interruption Insurance Coverage Act of 2020. The bill would mandate coverage for all business interruption policies and prevent the denial of claims due to major events like viral pandemics, forced closure of businesses, mandatory evacuations, and public safety power shutoffs.12 This bill allows insurers to deny coverage if premiums have not been paid. It does not specify that businesses must keep their staff employed or continue to cover their health insurance. Insurers have been critical of both the federal and state government bills; they state that the mandated coverage would result in ripple effects to the economy and could result in the insolvency of many insurance companies. The bill was referred to the House Committee on Financial Services at the time of writing.13

In light of the initial insurers’ responses, the federal government introduced other potential legislative business interruption solutions, including the Pandemic Risk Insurance Act (PRIA) on May 27, 2020,14 and the Never Again Small Business Protection Act of 2020 on April 14, 2020.15 Both bills have been introduced into Congress and await further action. 16

PRIA is a government reinsurance program, similar to the Terrorist Risk Insurance Act (TRIA), in which the US federal government would cap the total insurance losses an insurer could face. Insurers would elect to participate in PRIA and would provide insurance coverage for any future “covered public health emergency.”17 PRIA would apply to any insurance company licensed in any US state, territory, or possession, as well as any insurance company eligible to write insurance in the US on a surplus line basis. Insurers participating in PRIA would be subject to individual and industry deductibles. Insurers involved in PRIA would share losses up to $250 million, and the federal government would provide a backstop, after meeting certain deductibles, for up to $750 billion.18

The Never Again Small Business Protection Act is another piece of legislation designed to relieve the economic pressures small businesses face. The act would require that business interruption insurance provide coverage for losses of businesses and nonprofits that stem from any federal, state, or local government-ordered business shutdown following the declaration of a national emergency.19 The coverage would apply to businesses that have been impacted at least thirty days as long as businesses keep their employees employed and maintain their health insurance coverage. Insurers would only be able to exclude coverage if the insurer has received a written statement from the policyholder that affirmatively authorizes the exclusions.20 Policyholders would be excluded for failure to pay premiums associated with the coverage. The US federal government would implement a backstop to cover the costs of insurers providing coverage to small businesses in order to provide stability to insurers.21

1https://www.insurancejournal.com/news/national/2020/04/08/563723.htm

2https://legiscan.com/NJ/bill/A3844/2020

3https://www.njleg.state.nj.us/2020/Bills/A4000/3844_I1.HTM

4https://www.nysenate.gov/legislation/bills/2019/a10226/amendment/a

5https://www.legis.state.pa.us/cfdocs/billInfo/billInfo.cfm?sYear=2019&sInd=0&body=H&type=B&bn=2372

6https://www.legis.la.gov/legis/BillInfo.aspx?s=20RS&b=HB858&sbi=y

7https://www.legislature.ohio.gov/legislation/legislation-status?id=GA133-HB-589

8https://malegislature.gov/Bills/191/SD2888

9https://www.scstatehouse.gov/sess123_2019-2020/bills/1188.htm

10See bill links for status and https://legiscan.com/NJ/bill/A3844/2020 for New Jersey

11https://www.hklaw.com/en/insights/publications/2020/04/proposed-covid19-related-business-interruption-and-property

12https://www.jdsupra.com/legalnews/legal-and-regulatory-developments-75994/

13https://www.congress.gov/bill/116th-congress/house-bill/6494?s=1&r=3

14https://www.claimsjournal.com/news/national/2020/05/27/297274.htm

15https://www.congress.gov/bill/116th-congress/house-bill/6497/actions?r=1&s=1&KWICView=false

16https://www.claimsjournal.com/news/national/2020/05/27/297274.htm and https://www.congress.gov/bill/116th-congress/house-bill/6497/actions?r=1&s=1&KWICView=false

17https://www.insurancejournal.com/news/national/2020/05/27/570002.htm

18https://www.insurancejournal.com/news/national/2020/05/27/570002.htm

19https://www.jdsupra.com/legalnews/legal-and-regulatory-developments-75994/

20https://fitzpatrick.house.gov/media-center/press-releases/fitzpatrick-cisneros-hurd-suozzi-introduce-landmark-bipartisan-business

21https://www.jdsupra.com/legalnews/legal-and-regulatory-developments-75994/

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.

Published: 05/29/2020

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.