RubinBrown Sports Betting Index: December 2023 Analysis

RubinBrown Sports Betting Index: December 2023 Analysis

December Sports Betting Index (SBI)

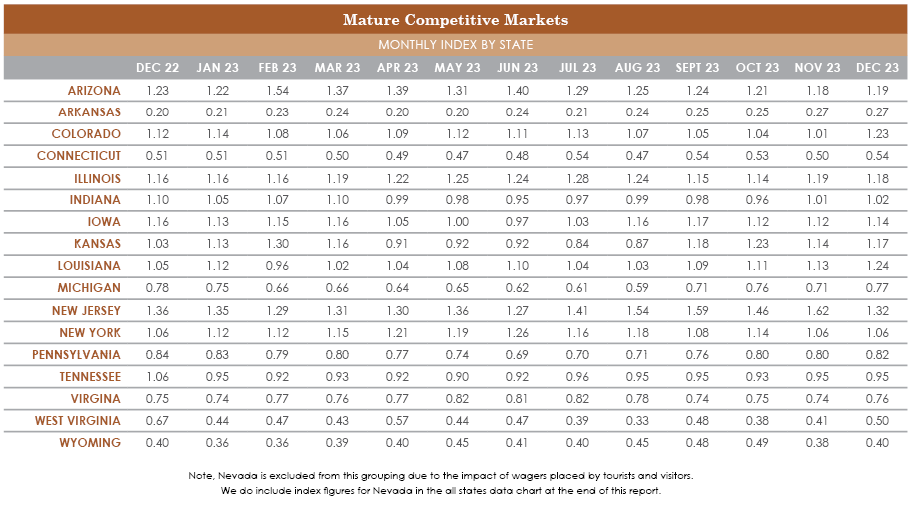

In the chart below, we present our RubinBrown Sports Betting Index (SBI). The SBI is based on our proprietary index of the leading sports betting states in the U.S. To continue to best reflect current market conditions, we’ll occasionally adjust the components of the index. To better compare competitive conditions, our index numbers focus in on a group of mature, competitive states. Therefore, a state with an index score of 1.15 had a raw index score of 15% greater than the average, while a 0.90 index score shows a 10% lower than average result.

Almost 3 months into 2024, we can finally close the books on 2023 with the last few states finally reporting their December sports betting results. In contrast to the continued growth of top line handle and revenues, our SBI shows a relatively flat marketplace. We find that much of the growth has been aided by a growing overall economy, the addition of new markets, and the maturing of markets which opened in 2022.

When analyzing results, especially yearly results, the RubinBrown Sports Betting Index has an advantage over other measures in that our index adjusts for macro level economic changes and market conditions. As these macroeconomic measurements change, we found that the industry needs a gauge of sports betting’s relative performance to supplement our understanding of the commonly discussed raw figures.

According to the US Census Bureau, per capita incomes in 2023 were estimated to be up 20% in many urban/suburban areas compared to 2022. The increase has been attributed to adjustments related to inflation and economic changes as the post-pandemic economy took shape. While most people probably didn’t have 20% more disposable income in 2023, the continued broad economic growth and improvements in income at all income strata likely provided a tailwind for sports betting activity which hopefully continues into 2024.

As pointed out in last month’s SBI, we are focused on handle for our analysis. Operators can influence GGR (gross gaming revenue) with their unique pricing and product offerings, and event outcomes are beyond anyone’s control, so handle is the more useful comparison of overall market health. However, we recognize that revenues continue to show higher rates of growth compared to handle as the move towards wagers with a higher hold, especially parlays, continued unabated in 2023.

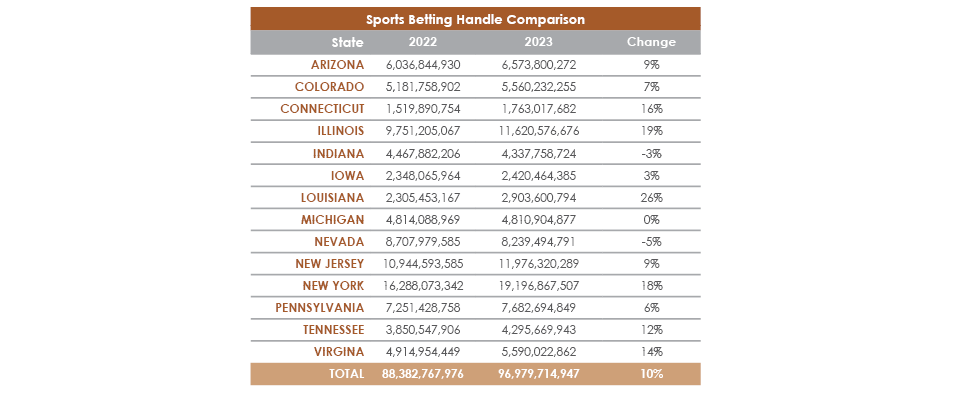

We noted the decline in handle in Nevada in our last edition (a trend which may see a bit of a reprieve thanks to the reported record handle on the Super Bowl). As we compare average index figures for 2022 vs 2023 in the larger markets that have been open since 2021, we see weak or generally flat performance in other states just Nevada.

The question we attempt to address is, have states attained 2023 sports betting handles that keep pace with economic factors and market conditions through 2023? Upon review of several mature, competitive markets with over $1 billion in handle, we found mixed results.

.png "DEC-SBI-MarketGrowth-(3).png")

Our brief summary of thoughts on the data include seeing more recently opened markets powering growth in both New York and Louisiana, both of which opened during January 2022 and therefore did not have the benefit of a fully ramped market throughout 2022, which made their 2023 perhaps a bit more impressive. Our most surprising states were Illinois, Connecticut, and New Jersey. Illinois appeared to have a solid summer and followed it up with a good fall with no apparent new drivers. New Jersey’s strength we touched upon in a recent SBI report as having been one of the strongest performers of the fall despite New York showing no concurrent signs of weakness.

On the more disappointing side, we had Michigan, which may have lost some patrons to openings in Ohio and Ontario. Even if there was some small loss of patrons to newly opened sports betting markets, the state continues to see a far weaker general SBI that we believe may be somewhat attributed to online casino availability. Two more established sports betting-only states, Indiana and Nevada, were also the laggards in 2023. Nevada we touched on before but Indiana might have seen some loss to Illinois for some unclear reason, as well as some potential losses to new openings in Ohio and Kentucky.

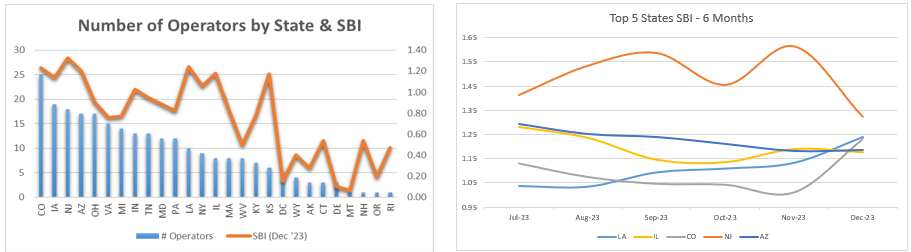

We do foresee the continued opening of new markets, which will potentially sustain industrywide handle growth for another few years, but the closure of some sportsbooks combined with most markets dominated by just a couple of operators would suggest that declines could spread to more markets. The landscape will continue to change as these types of conditions usually lead to attrition followed by consolidation. The attrition phase has been upon us for a while. With M&A activity starting to heat up, the consolidation phase is probably not far from arriving.

As existing markets continue to mature and new markets legalize, we will continue to monitor the progress of sports betting handle as it relates to both the state level economics and the broad economy. Our index will pinpoint those states that were keeping up with the improving economic and market conditions as well as identify those who aren’t.

Published: 02/28/2024

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.