RubinBrown Sports Betting Index: November 2024 Analysis

RubinBrown Sports Betting Index: November 2024 Analysis

November Sports Betting Index (SBI)

In the chart below, we present our RubinBrown Sports Betting Index (SBI). The SBI is based on our proprietary index of the leading sports betting states in the U.S. To continue to best reflect current market conditions, we’ll occasionally adjust the components of the index. To better compare competitive conditions, our index numbers focus in on a group of mature, competitive states. Therefore, a state with an index score of 1.15 had a raw index score of 15% greater than the average, while a 0.90 index score shows a 10% lower than average result.

LEARN MORE ABOUT THE RUBINBROWN SBI

When all of the numbers are reported, November sports betting handle should eclipse the $16 billion mark for the first time as players continue to flock to the proverbial windows. In the coming months, we do expect seasonality to begin to moderate results, with the first signs occurring in November numbers. While most mature/competitive states continued to show MoM improvements, several states, including New York, began to show seasonality with their first monthly handle decreases since August. Even with a modest handle decrease, the Empire State was still able to post a record GGR total of over $232 million on a 10.21% hold, surpassing their previous high of $211 million in January of 2024.

Thoughts on the new “Subscription Model”

The industry will be very interested to see the effects of DraftKings’ newly implemented subscription-based offering in NY, where players can boost parlay bet payouts if they subscribe to a monthly subscription service. Priced at $20 per month, DraftKings launched the new service in December. The service offers “stepped-up” odds boosts on all parlays where individual legs are at least -500. For parlays with two legs, patrons will see their winnings increased by 10%. As more legs are added, the boosts increase. Parlays with 11 or more legs can receive a 100% increase.

We believe this new product aligns with DraftKings and other sportsbooks’ strategic goal of increasing the share of all wagers placed on parlays and the average number of legs included on each parlay. Kicking off the strategy in the state with the highest tax on GGR (51%) is not a surprise. Subscription-based revenue is generally not considered taxable gaming revenue, and boosted parlay payouts will decrease GGR and taxes paid. Therefore, this move could increase realized net profit. If successful, we would expect this to be offered in other states and for competitors to offer their own versions of a subscription model.

Our back of the envelope math based on DraftKings November 2024 results, conservatively assuming parlays account for 25% of handle and have a 20% hold, suggests they will be successful if they maintain at least 90,000 subscribers. The benefits of the subscription plan also go beyond changing customer activity and the potential tax benefit. This could also increase customer “stickiness” and loyalty. For subscribers, the upfront payment likely creates an incentive for increased play as these customers aim to get their $20 worth in value each month, while also possibly deterring the motivation to shop for better prices at competing sportsbooks.

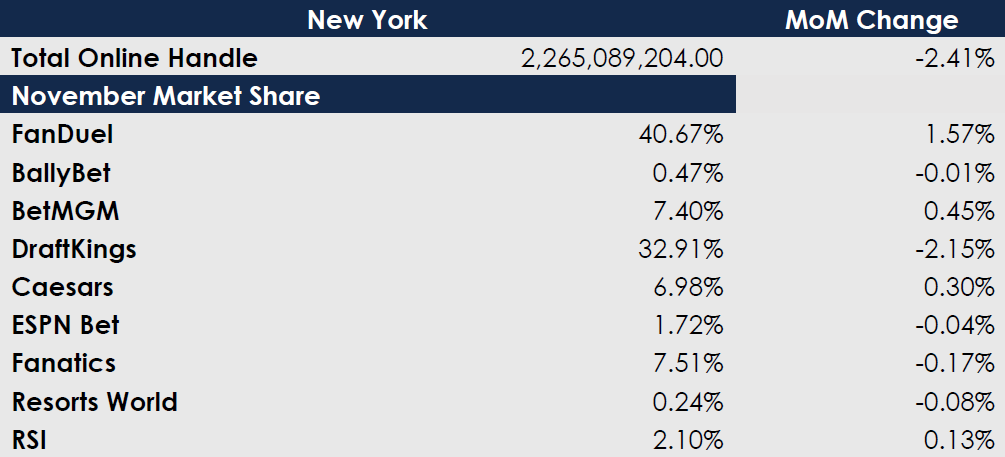

New York’s November market share for the leading operators can be found below. Contact us for more information regarding this analysis.

.png "November-2024-SBI-(1).png")

MO Online Sports Betting Timeline

Missouri is moving quickly through the regulatory process to become the latest state offering regulated online sports betting to patrons state-wide, with the possibility of “emergency” rules being sent to the Governor by the end of January. With 38 states already having legalized some form of regulated sports betting, Missouri benefits from the opportunity to learn from the experiences of other jurisdictions and streamline its regulatory process.

Upon the approval of emergency regulations, the state can commence the licensing process. A total of 21 online sports betting licenses will be available, although it is unlikely all licenses will be utilized over time. Latest expectations indicate the first bets are likely to be placed sometime in the summer.

Published: 01/22/2025

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.