COVID-19: Economic Injury Disaster Loan, Paycheck Protection Plan Loan or Both?

COVID-19: Economic Injury Disaster Loan, Paycheck Protection Plan Loan or Both?

Businesses and organizations have various loan options available to help offset financial hardship and uncertainty caused by the COVID-19 pandemic. This article compares two of the most talked about loan programs, the Small Business Association (SBA) Economic Injury Disaster Loans (EIDL) and the Paycheck Protection Program (PPP) loan.

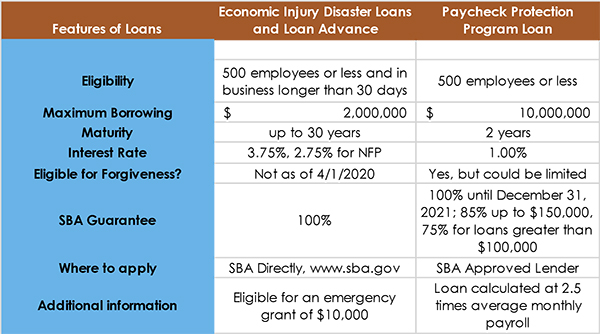

A summary of both the EIDL and PPP loans is shown below:

What makes the EIDL more advantageous than the PPP loans?

The two largest benefits for the EIDL are the extended terms of the loan and access to the $10,000 emergency tax-free advance which is 100% forgiven at the time it is advanced. Even though the interest rate is higher, 3.75% for EIDLs vs 1% for PPP loans, the term of the EIDL is up to 30 years vs the two (2) years of the PPP loans. If you expect your organization to have a slow return to ‘normal’ operations out of this pandemic the EIDL might be more advantageous. An additional benefit of the EIDL is that the proceeds of the loan can be used for all operating costs, unlike the PPP loans that must be used essentially only for payroll cost, rent, utilities, and interest payments.

What makes the PPP loans more advantageous than the EIDL?

The first thing that gets people’s attention is the forgiveness portion of the loan. The true purpose of the PPP loan is to help small business owners retain and pay their employees. The PPP loan provides employers with access to funding to cover 8 weeks of their payroll costs. The benefit is that organizations can repurpose funds originally earmarked for payroll to keep their organization operating. This affords employers the ability to focus on their organization and try to maintain or, if possible, position themselves for growth coming out of the pandemic.

When should I pick the EIDL?

If your organization currently has a significant reduction in payroll as a result of the stay at home order, and you do not feel the company will be re-opened and back to pre-pandemic staffing levels, then the EIDL may be more advantageous. In addition to the lower amount of eligible forgiveness under the PPP loan, the shorter payback period could strain your working capital once you reopen. Also, if you need the loan proceeds for operations other than payroll, the EIDL provides more flexibility and longer repayment terms than the PPP loan. The EIDL can be applied for directly with the SBA, there is no need to find a SBA approved lender.

When should I select the PPP loan?

If your employee count is higher now that it was in second quarter 2019 or January and February 2020 it is fair to presume that you will receive a significant amount of the eligible forgiveness of your PPP loan. Couple the loan forgiveness (tax free by the way) with the benefits of retaining your workforce during this difficult time and your organization should be set up to do well post-pandemic. The application of the PPP loan is also simpler and payment of the loan proceeds should happen sooner than the EIDL.

Can you apply for both loans?

The SBA is clear in that it does allow for both EIDL and PPP loans to be awarded for the same organization. However, the loans cannot be used for the same purpose. Meaning you cannot take out both loans to fund payroll. Per the SBA, you would be authorized to take out a PPP loan to fund payroll and then the EIDL to fund inventory that is delayed due to the effects of COVID-19, for example.

PPP Loan vs. EIDL Survey

RubinBrown would like to get your feedback regarding the PPP loans and EIDL. We invite you to participate in our confidential survey regarding these programs. View the live results below.

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.

Published: 04/09/2020

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.