Focus on Lease Accounting: Classification and Expense

Focus on Lease Accounting: Classification and Expense

The previous articles described the scope of the standard, the definition of a lease, identifying components and determining the lease liability and right-of-use (ROU) assets. Similar to the legacy accounting guidance, ASC 842 requires the classification of leases. Under ASC 842, a lease is a finance lease when any of the following are met at lease commencement:

- Ownership is transferred by the end of the lease term

- Lessee is expected to exercise purchase option

- The sum of i) PV of lease payments and ii) any guaranteed residual value approximate or exceed the fair value of the asset

- Lease term is for major part of the remaining economic life of the asset

- The underlying asset is of such a specialized nature that it is expected to have no alternative use

Leases that do not meet any of the criteria would be classified as operating leases.

The new rules include language that mirrors the legacy criteria with the addition of the consideration of the specialized nature of an asset. Additionally, the basis for conclusions indicates that “one reasonable approach” to classification would be to conclude that a finance lease results if either:

- The lease term is equal to 75% or more of the remaining economic life of the leased asset, or

- The present value of lease payments (plus any residual value guarantee) equals or exceeds 90% of the fair value of the leased asset.

Given the similarity in the requirements, lease classifications are not expected to change significantly upon adoption of ASC 842.

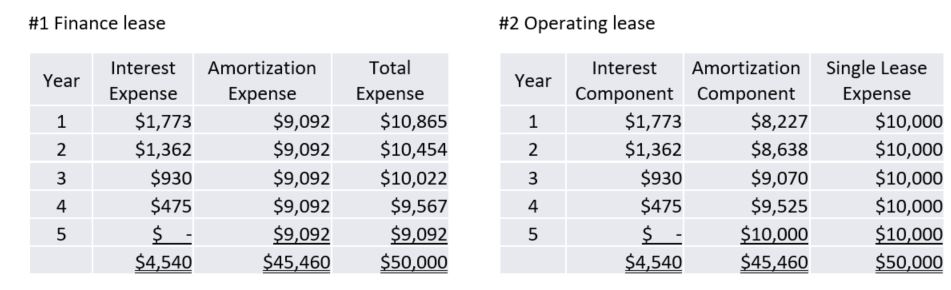

As discussed in a previous article, the initial accounting for a lease is the same, regardless of the classification. A lease liability for the present value of lease payments and an offsetting ROU asset are recorded, with some potential adjustments. The classification will result in different patterns of expense recognition. For a finance lease, interest expense is recognized separately as a finance cost, with the ROU asset amortized straight-line over the lease term, resulting in a front-loaded recognition pattern. An operating lease is expensed as a single lease expense on a straight-line basis over the lease term. To achieve this, the interest is amortized normally and the amortization of the ROU asset is essentially a plug to get to straight-line in each reporting period.

Consider the following examples:

In either case, the accounting on commencement date is the same:

Dr. ROU Asset $45,460

Cr. Lease Liability $45,460

The first lease payment is also on commencement date and would be recorded as follows:

DR. Lease Liability $10,000

Cr. Cash $10,000

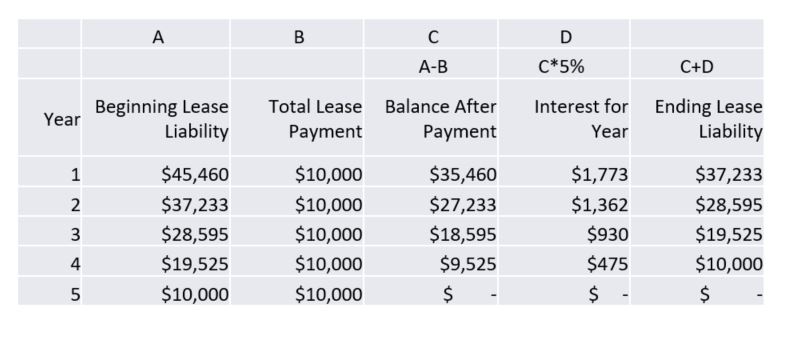

The amortization of the lease liability is also the same for both types of leases:

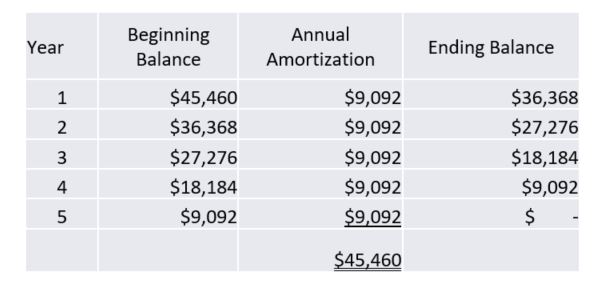

For a finance lease, the ROU asset amortizes on a straight-line basis:

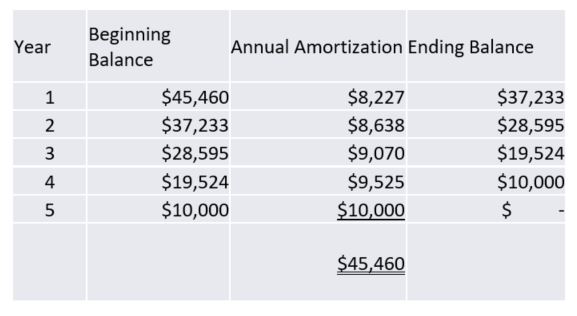

Operating lease ROU assets amortize so that total expense is straight-line:

The total expense by year will differ by type of lease. Total finance lease expense is accelerated; total operating lease expense is straight-line.

In the next installment, we will cover a variety of topics including modifications, impairment and the enhanced disclosures required under the new standard.

Readers should not act upon information presented without individual professional consultation.

Published: 07/12/2021

Readers should not act upon information presented without individual professional consultation.

Any federal tax advice contained in this communication (including any attachments): (i) is intended for your use only; (ii) is based on the accuracy and completeness of the facts you have provided us; and (iii) may not be relied upon to avoid penalties.